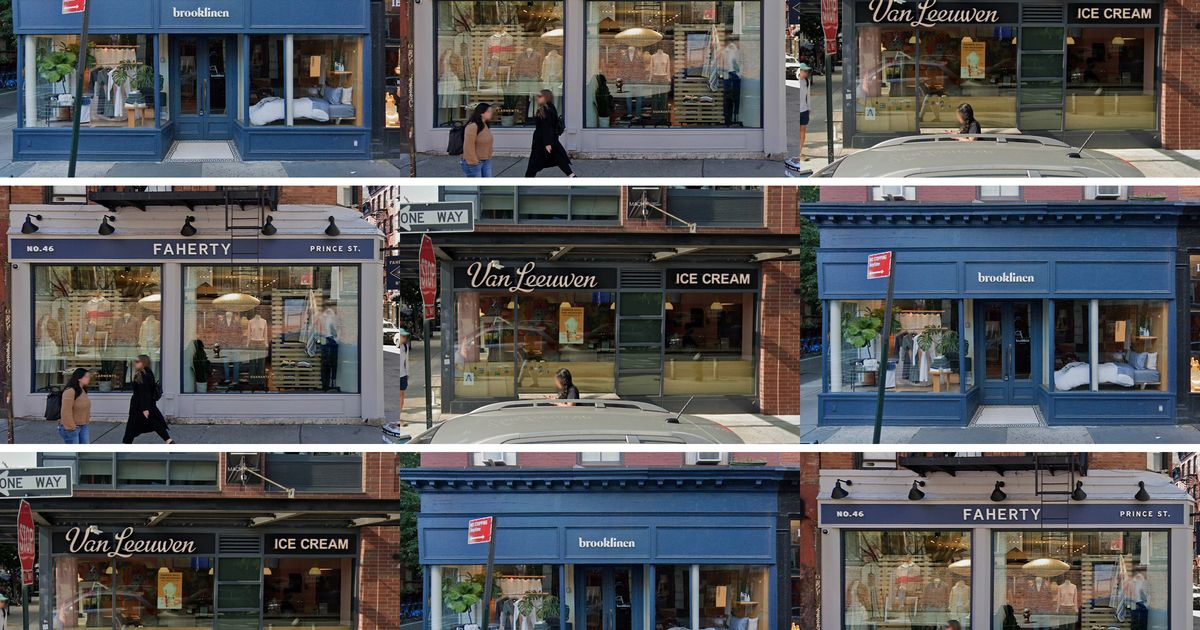

Chain retail clustering creates cookie-cutter neighborhoods across American cities. Luxury boutiques like Aesop, Everlane, and Buck Mason now anchor the same streets in different markets, turning distinct neighborhoods into interchangeable shopping districts.

This phenomenon reflects how real estate developers and retailers operate. Anchor tenants drive foot traffic and command premium rents. When one upscale brand leases space, others follow quickly. Landlords recognize the pattern works and pitch the same tenant mix to new projects. The result: SoHo looks like Nolita looks like Brooklyn Heights.

For property owners, this clustering boosts foot traffic and justifies higher rents. A 2,500-square-foot retail space in a mixed-use development with Aesop and Everlane nearby commands $100 to $150 per square foot annually in major metros. Without anchor tenants, comparable space rents for $40 to $60.

But the strategy erodes neighborhood character. Local independent boutiques cannot compete with chains that operate dozens of locations simultaneously. They lack the capital to match buildout costs or advertising budgets. Rents climb. Independent operators leave. Sameness replaces authenticity.

Consumers notice. Shopping districts feel generic. The boutique that made a neighborhood distinctive vanishes. Residents seeking unique retail experiences travel farther or shop online.

For residential real estate, this matters. Neighborhoods marketed on "walkable, vibrant retail corridors" increasingly deliver the same stores everywhere. Buyers paying premium prices for location-specific charm discover they could visit the same shops in three other cities. Rental appeal weakens when the neighborhood experience becomes replicable.

Developers defend the approach. Chain retailers commit to longer leases and pay predictable rent. Independent owners negotiate annually, creating uncertainty. From a pure capital perspective, clustering works. Leasing teams book